Last updated April 2026

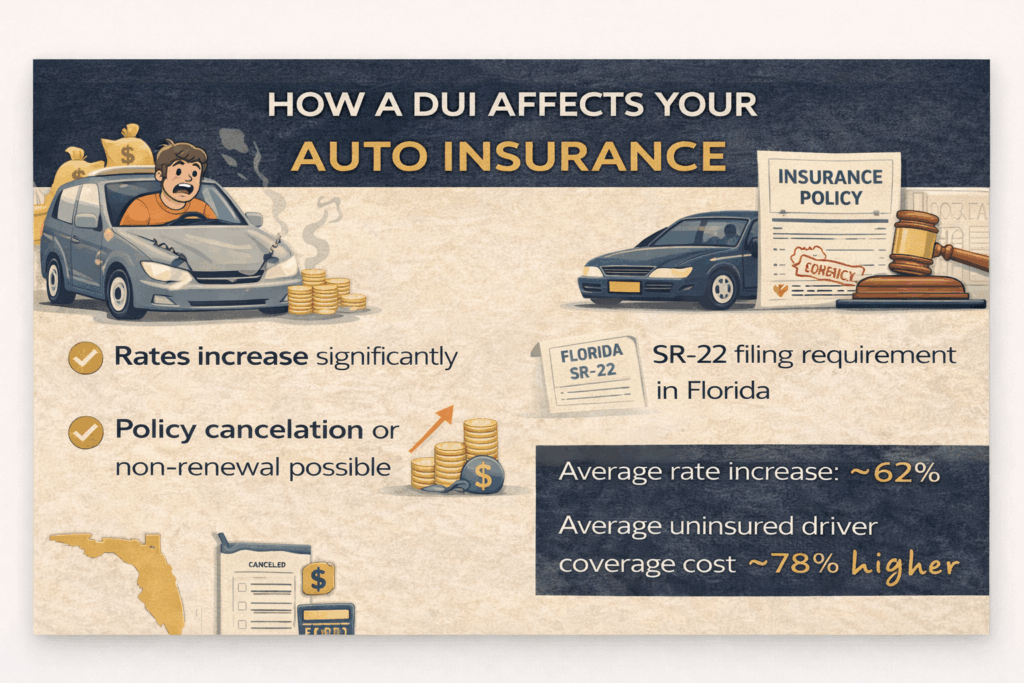

One of the most common questions after a DUI case in Florida is: “What happens to my car insurance?” While an arrest alone does not automatically trigger Florida’s high-risk insurance requirements, a DUI conviction can significantly increase premiums and impose new compliance obligations to keep a valid driver’s license.

This guide explains what typically happens to insurance after a DUI conviction in Florida, including rate increases, FR-44 requirements, and how policy lapses can lead to immediate license consequences.

For a broader overview of what happens after a DUI conviction — including financial, legal, and long-term consequences — see our guide to DUI Consequences in Florida.

📈 Will Your Insurance Go Up After a DUI in Florida?

If you are convicted of DUI in Florida, your auto insurance premiums commonly increase substantially—often doubling or more depending on:

-

Prior driving record

-

Whether the DUI involved an accident

-

Whether this is a first offense or repeat offense

-

Overall risk classification by your insurer

Higher premiums often last for several years, especially when the conviction triggers high-risk insurance requirements.

📄 What Is FR-44 Insurance in Florida?

After a DUI conviction, Florida requires many drivers to carry an FR-44 (a certificate of financial responsibility) in order to reinstate and maintain driving privileges.

FR-44 generally requires higher liability coverage limits than standard policies. Insurers file FR-44 documentation with the Florida DHSMV to confirm that the required coverage is in place.

These requirements often come into play alongside license reinstatement procedures and other administrative consequences.

💰 What FR-44 Requires

FR-44 policies typically require at least:

-

$100,000 bodily injury liability per person

-

$300,000 bodily injury liability per accident

-

$50,000 property damage liability

Many drivers are required to maintain FR-44 coverage for at least three years following a DUI conviction.

⛔ What Happens If Your FR-44 Policy Lapses?

FR-44 compliance is strict. If the policy lapses or is canceled for nonpayment, insurers generally report the lapse to the DHSMV. This can trigger an immediate license suspension until coverage is reinstated and the FR-44 is re-filed.

Because of that, missed payments can create serious license problems even after the criminal case ends.

These requirements often arise alongside license suspension and reinstatement issues — see DUI License Suspension in Florida.

🧠 DUI Insurance Consequences Are Part of DUI Penalties

Insurance requirements, FR-44 compliance, and license reinstatement costs are part of the broader consequences that can follow a DUI conviction — which are imposed through the sentencing process explained in our guide to DUI Sentencing in Florida.

❓ FAQs: DUI Insurance and FR-44 in Florida

Q1: How much will my car insurance increase after a DUI in Florida?

Most drivers in Fort Lauderdale and South Florida see their auto insurance rates double or triple after a DUI conviction. The rate increase usually lasts 3 to 5 years.

Q2: What is an FR44, and why do I need one?

A: An FR44 is a certificate of financial responsibility required after a DUI conviction. It proves that you carry higher liability insurance, and it must be filed to reinstate your driver’s license.

Q3: How long do I need FR44 insurance after a DUI in Florida?

A: Most drivers are required to maintain FR44 coverage for at least 3 years after their DUI conviction to remain legally licensed.

Q4: What happens if I miss a payment on my FR44 insurance?

A: If your policy lapses, your insurance company is required to notify the DMV, which will suspend your license immediately until the policy is reinstated and the FR44 is refiled.

Q5: Do I need FR44 if I was only arrested for DUI but not convicted?

A: No. The FR44 requirement is triggered only after a DUI conviction, not an arrest.